THE GLIMPSE GROUP IS NOT A COMPANY in the virtual reality and augmented reality space that some may have heard of before. Yet, the company is a bit of an emerging giant with over 200 people in offices from New York, Boston, and Dallas in the US to locations in Australia, Israel, and Turkey.

What makes The Glimpse Group special is its formation and structure, and position in the market. The company is a virtual and augmented reality platform company made up of multiple (13) subsidiaries focused on VR/AR software and services. It is also a publicly listed company on the Nasdaq (VRAR) and has rapidly growing revenues in the rapidly expanding immersive reality markets.

The VR/AR Markets

I had a chance to talk to Glimpse President and CEO Lyron Bentovim about the VR/AR markets and his company’s position in them a few weeks ago. His comments provide a large lens on the VR/AR industry, shedding light on such issues as VR/AR adoption rates, industry pickup, and when we reach mass adoption versus the phase we are in now. His comments and perspectives are a refreshing contrast to some of the things said about the industry by other leaders whose motivations may be quite different from that of Bentovim.

We are early in this industry, and enterprises tend to have specific needs for their activities and challenges. This is why we need to offer the ability to customize solutions to address their particular needs and challenges.

To unpack that last sentence, let’s begin with some key differences about The Glimpse Group. Glimpse does not make a headset. It does produce VR/AR software solutions but not the kind you and I would buy from, say, the web or an app store.

Glimpse offers “enterprise solutions” across an extensive range of industry sectors. From the client-side, the goal is simple—gain competitive advantages by leveraging Glimpse’s VR and AR innovations.

In the remainder of this article, we converse on a range of topics about VR and AR and his company and touch on such things as Apple’s play in this space.

The Interview

(AFR) I understand you have over 125 full-time developers, engineers, and 3D artists, but you are not creating a software platform. Can you explain where this expertise is being applied?

Lyron Bentovim (LB) Well, Glimpse is a platform company focused on enterprise VR and AR. We have 13 different subsidiaries, and each one of these subsidiaries has its own brand and its own technologies. Yet, they work together within the Glimpse eco-system, sharing knowledge, know-how, and IP.

So are you creating solutions from the ground up for your customers or using a mixture of off-the-shelf products? How does it work?

We offer software solutions, some of them are based on our off-the-shelf software but with customizations to the software. We are early in this industry, and enterprises tend to have specific needs for their activities and challenges. This is why we need to offer the ability to customize solutions to address their particular needs and challenges.

Having used VR myself in architectural practice, I can easily understand the need for custom functions. I am curious to know how your clients ask for customization—can you provide an example?

Customers tend to get the software solutions out there and want more. And because of how the industry functions—you put in a request for a feature and then wait to see if it ever happens—we can go in and develop that feature now and integrate it into their workflow.

Advertisement

For example, a customer in education had a feature with a whiteboard but wanted their students to have a mobile whiteboard. The customer could wait for it, and maybe it would appear in a year, or they can hire us, and we deliver it to them just the way they want it in the present time frame.

Do you have partnerships with the VR headset companies?

Yes. We work closely with all major headset manufacturers, from Meta (Quest) and Pico, to the tethered ones like Varjo and HP. From our view, we want to know what is coming out ahead of time before end-users do and manufacturers want to work with us because they want our software solutions to be successful so they can get their headsets in front of our enterprise clients.

That seems like a clear win-win strategy for everybody, especially your customers. Where do you see the greatest amount of traction on the AR side of the market?

It is definitely a win for our customers as we can deliver the leading edge for their particular needs. As for traction in AR, it is in the marketing industry in the short term.

Brands are trying to reach that very elusive GenZ type demographic. And they can’t find them anywhere where they used to find people like you and me. They are not in any of the standard advertising channels, nor the new standards like Facebook and stuff; they are not there either.

The Millennial and GenZ generations are much more open to AR/VR technologies and leading brands are using augmented technology, in particular, to reach these demographics in their marketing strategies.

So they need to find them where they are—places like TikTok, Snap, and Instagram. And they need to speak to them in their language, and this generation is engaging in AR.

So are you saying the millennials or GenZ are further down the line regarding AR adoption?

Yes. That is their willingness to engage with that technology.

You are specifically talking about their willingness to engage with that technology on their phones, correct?

Yes. AR on headsets like Hololens, MagicLeap, or industrial headsets like Vuzix and the likes—we are not seeing a lot of traction there. They are expensive, limited, cumbersome, and not very easy to make mass deployments. We are working with some of these companies and trying to help push their products out there, but the reality is AR on the phones is easy. Everybody has one.

Brands want to connect with their customers. They are activating [AR in] apps like Snap and Instagram—apps that everybody is already using—and engaging with those brands in a more immersive way.

Perhaps the marketing sector is taking off because you are working with very large Fortune 500 companies with the budget to explore edge-of-market technologies?

Yes, but working with those same customers on other areas of VR and AR, which I think is just as valuable if not more, and they don’t have the budgets there. And part of that is how budgets are allocated. So marketing budgets are a lot more controllable. And those organizations have a way of playing with them to achieve their goals. At the same time, for example, corporate training budgets are much more fixed.

How do you see the relationship of AR and VR to all the metaverse talk?

So the Metaverse is the endgame of these two technologies. I look at this as a 35-year tech cycle. And we are probably year seven or eight of those 35 years. And the end goal is the Metaverse, and there is no metaverse right now.

Yet, we can see the path that we are on. And the three technologies that are driving us towards the Metaverse are immersive technologies (like VR and AR), blockchain, and AI.

We and all the other companies in this space are all driving toward that goal of the Metaverse. Similarly, if you were to ask Microsoft in the early 90s how they saw their Internet plan, they would say they were focused on building solutions for their customers but also building the basic building blocks to enable them to continue to do that as the technology changed—from having a presence on the Internet, selling things on the Internet, to having cloud solutions on the Internet, which is a significant piece of Microsoft’s business right now. You couldn’t do that last part in the 90s because the technology wasn’t there yet.

I look at this as a 35-year tech cycle. And we are probably year seven or eight of those 35 years. And the end goal is the Metaverse, and there is no metaverse right now.

In many ways, it is the same. We are building solutions for our customers that are very standalone in their nature. The Metaverse will come and enable all of these things to connect, and you will be able to move between these experiences. But right now, the building blocks we are building for our customers will enable them to excel as the world around them evolves.

That is a thought-provoking analogy. Of course, there are a lot of companies talking a lot about the Metaverse right now, like NVIDIA.

NVIDIA, in my view, is going to be one of the biggest winners of this space. Firstly, they get it in a way that I think most others don’t. Secondly, they are constantly thinking of their technologies in a way that will bring the new into the old as they are replacing themselves.

The Metaverse will offer numerous new possibilities for markets. At the moment AR/VR technologies are finding numerous simulation, training, and coaching applications like this one serving the data market.

So NVIDIA already is in a dominant position because its chips are inside most of the hardware driving this business. Yet, that’s not enough for them. They understand that the GPU is limited in these types of headsets with power limits. So they are developing the technology to have the immersive experience powered in the cloud, and you just stream that experience to the user.

That relationship between hardware power and devices is a tricky one and probably the reason why Apple has taken so long to develop an AR or VR headset.

And also, the displays are another area. The triangle of technologies is the display, the computational power—particularly on the GPU side—and the form factor; that triangle has not been solved yet.

Advertisement

The form factor is tied to power because you can’t get things small enough yet since you are trying to be untethered i.e. not connected to a computer. And Apple is a perfectionist company, so they won’t release something that is just ‘okay-ish’; they will wait to release something until it is great.

Many people think it will take Apple to get the masses really excited about these VR/AR technologies. Do you agree that they can mass popularize VR and AR?

Yeah, I agree with that. I look at the history of technology cycles. The first half of a technology cycle is hardware, where the evolution in hardware drives the business until you get to the point where there is mass adoption. But we are so far from the point of mass adoption because the hardware isn’t there yet.

Because that triangle of tech hasn’t been mastered yet?

Yes. The hardware is good for people who want to experiment and learn how this would work, but it’s not there for mass adoption both on the consumer and business sides.

The triangle of technologies is the display, the computational power—particularly on the GPU side—and the form factor; that triangle has not been solved yet.

When Apple comes in, that might be the tipping point in that direction, and it might take a few more years after that. I feel we are five to seven years away from what I call mass adoption. Then we will change the other half of the cycle; it will become a software game, and we will be ready for the Metaverse because we will have everybody there.

Let’s talk about AEC. I know this was one of the first industries with significant promise with VR/AR. It began about seven years ago. But the actual take-up in the industry appears to be much smaller than I would have imagined it. What is your take on VR/AR in the AEC industry?

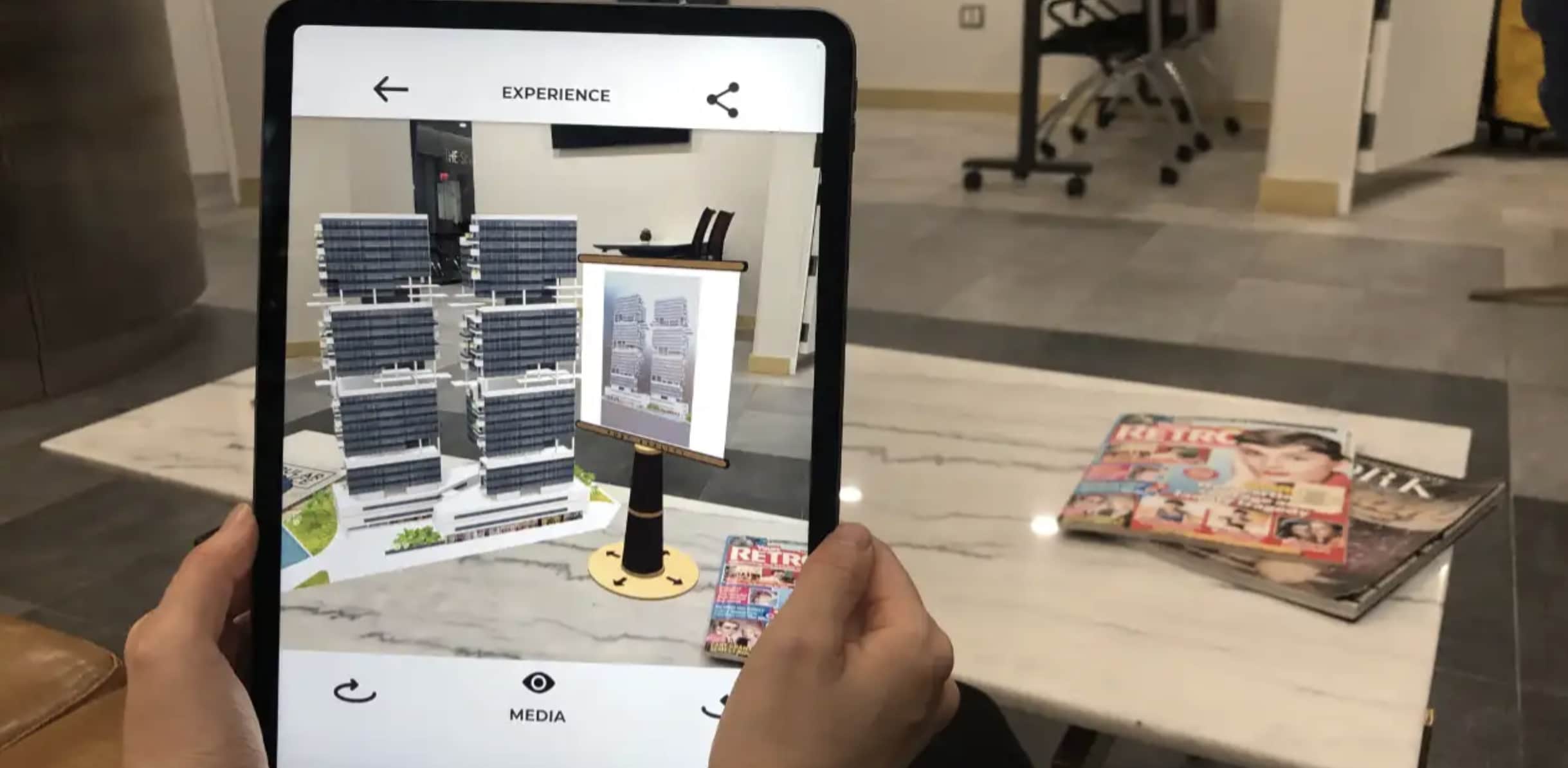

You raise an interesting point. The AEC industry is probably one of the most frustrating in terms of lack of adoption. It baffles me on why. The industry would benefit significantly from being able to visualize and use those [VR/AR] tools.

Augmented reality (AR) tools are gaining ground in the AEC industry. This shows a user looking at a virtual building in 3D complete with a virtual computer screen also showing the building (like in a presentation mode). Pass-thru video merges the real environment of a marble table in a room with these virtualized elements.

We have worked with architecture and construction firms and with real estate firms. Yet, a lot of that work has been very limited. And while each engagement was successful in reaching the goal, we haven’t managed to get that to move from one or two implementations to, ‘let’s now make this as how we do things.’

Despite the apparent successes, it hasn’t taken off, and I’m not sure why. Given the number of dollars and the amount of savings through these efficiencies, it should take off. It’s baffling. Let me throw the question back at you, why do you think it has not taken off other than these are conservative industries?

Unfortunately, the AEC space is a laggard in information technology adoption. The percentage of revenues going into digital technologies in AEC is around 1.5 – 3.5%, with construction firms on the lower end. That pales compared to other industries.

The construction industry has been newly focused on digital tools, particularly tools that solve time and labor-constraint issues. There is a knowledge-transfer issue in the construction industry. Ironically, this is where I can see AR and VR playing a role. You have all this expertise locked up in the minds of veteran construction pros. So the short-term goal is to keep them working, but that is not a long-term solution.

The AEC industry is probably one of the most frustrating in terms of lack of adoption. It baffles me on why. The industry would benefit significantly from being able to visualize and use those [VR/AR] tools.

Then there is AI being deployed to solve the workforce shortage—cameras, robots, remote observation, safety monitoring—all designed to deal with less available experienced boots on the ground.

As you know, the Covid crisis did usher in increased demand for VR and AR tools because you couldn’t get places. The Wild, which was acquired by Autodesk recently and a company we know well, explained to us in a report how Covid accelerated the take-up of VR.

So that is my snapshot. So compared to AEC, how do you see manufacturing’s take-up in VR and AR technologies, especially AR technologies? So this spans from Vuzix to industrial-grade tools like Varjo used in automotive and aerospace. I am sure you are familiar with the latter.

Varjo is incredible, but they are costly. You are talking three thousand dollars for just the Varjo headset and then another three thousand for the hardware to run them.

You use that technology when you want to showcase a helicopter instead of bringing the helicopter in; you can use that technology and do very high-end simulation work. So Varjo works when you need a few locations at a very high value. You can’t give that kind of technology to many workers; that’s very high-end and expensive gear. That is the drawback with them.

Virtual and augmented reality are already becoming crucially successful in the aviation and automotive industries—essentially serving the transportation revolution technologies like EVs, vertical take-off and landing (VTOL) vehicles, Hyperloop, and traditional air and auto markets.

So in the manufacturing and industrial sectors, there is a distribution challenge. On the low end, you have a Quest which is three hundred dollars, and mobile and doesn’t need anything else. It’s not as beautiful as Varjo, and once you have gone to Varjo, it is hard to go back to the Quest—it’s like experiencing color TV and then expecting to go to black and white TV. But Quest is the price point where you can deploy at scale.

So there will likely be some high-end markets with few contact points. And Varjo is solving problems like flight simulation that are less expensive to solve than limited actual flight simulators, which are factors more expensive. But you are saying that the low-end gear will increase and tackle more professional problems.

Yes. And the high-end will become the new low-end, and you will have the usual technology maturity and ‘good enough’ break points in the technology cycle, just like with computers over their long history.

That is just how technology works. The high-end shows us where we are going.

Lyron, thanks for talking to me about The Glimpse Group and your invaluable perspectives on VR and AR now and in the near future.

You are welcome.

Reader Comments

Comments for this story are closed